Top 10 Tips To Running Your Own Business

The Idea

Put a lot of energy into your business idea

Things to think about

Is my business a new start up

Have I bought the goodwill of an existing business

How am I going to turn it from an idea to a real working business

What type of business is it.

How am I to market the business

Do I have the necessary skills to make it work

Do I need the help of others

Do I need premises or can I work from home

How saturated is my market, how can I stand out from the crowd

Low cost price/versus high volume

High cost price/versus low volume

Services/Product mix

Costings of the service/product

Your USP

Unique Selling Point

Why should a potential customer buy from you?

Put together a plan detailing your USP and start promoting this from day one. This can change over a period of time as your business develops.

Think about your branding at this stage. You want to be familiar make it stand out.

Put together a business plan

I spend a lot of time mentioning putting together a business plan. It will focus the mind and highlight any potential issues you make have to face and overcome. The financials and the competition being the main parts of the plan. Spend a lot of time on these and you will have a well thought out plan ahead for you to work to.

Soletrader, Partnership or Limited

Tax relief available for Limited, but increased paperwork. Decide your status at the beginning of the life of the business. It can change at a later stage as it needs to.

The Cashflow

In the early days you will find yourself paying out and not seeing the instant reward for a period of time. Put this together with open eyes. The Sales income may be slow to start off with.

Put together a simple cashflow and complete with actuals month on month, and always roll it ahead. You can see instantly where your surplus/deficit cashflow is.

Goal Setting or KPI’s

Set yourself some goals to achieve in year 1, 2 and 3.

Sales targets

Gross margin

Net profit

Sales enquiries/website traffic

Segmentation i.e. sales types split up by category versus margin from each type

Whatever you decide to choose, keep this in both numerical format and graphical format and compare month on month, year on year. You can see instantly that you either are going the right way, or need to take action to get back on track.

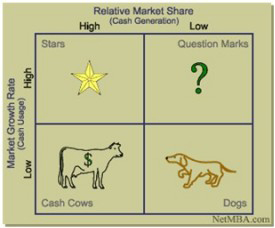

The Competition

Always stay one step ahead of the competition

Review key words on the web

Price testing of the market

USP

Value for money

Unique product/service

Find out what the competition are doing and stay up to date. Look at both the smaller companies (they tend to grow) and the larger companies. (they may have a bigger marketing budget) you can learn from them. They were small once.

Your Customer

Know your market inside out. This needs to be specific, not too general.

The demographics. Is your business local or can it be national or international.

Age group, gender

Financial budget of the customer you are targeting

Seasonality

By knowing your customer you can sell to them better.

Get a website

Not all businesses need a website but most need a web presence of some kind. Look into your competition if they have a website then you need one too.

There are many low cost examples to start off with, and as you get bigger this can be something you can develop over time.

Accountant

Keep your accounts in good order and you will always know where you are financially. It is key to know you’re making a profit and staying that way.

Taking action if your finances need a pick me up.

Use your Accountant as someone who you can telephone from time to time to discuss your strategy. It should be a two way street.

It’s not just about preparing tax returns and accounts, this should be part of your strategy.

This blog is intended for information purposes only and is only advice from past experience, you may have other suggestions of your own. It is not intended to be used to make all of your business decisions but as a guide only.

FREE initial consultation – call 02920 653995 (Cardiff) or 01656 530063 (Bridgend) or email hello@crossaccountingservice.co.uk for an appointment.

FREE initial consultation – call us on

02920 653995 or 01656 530063